The natural foundations for human prosperity are being undermined at an alarming rate, yet according to the UN Convention on Biological Diversity (CBD) the financial solutions currently on the table will be insufficient to halt or reverse the decline. We argue that an agreement to revise the terms of existing and new fixed income instruments would provide a short term solution.

The UN CBD Global Biodiversity Outlook 5[i] has found that none of the 2011-2020 Aichi Biodiversity Targets have been met, with only six being partially achieved. Across sixty indicators such as habitat loss, sustainable fish stock management, preventing harmful pollution, protecting the world’s land and sea, and boosting finance for nature, only seven (12%) have been met.

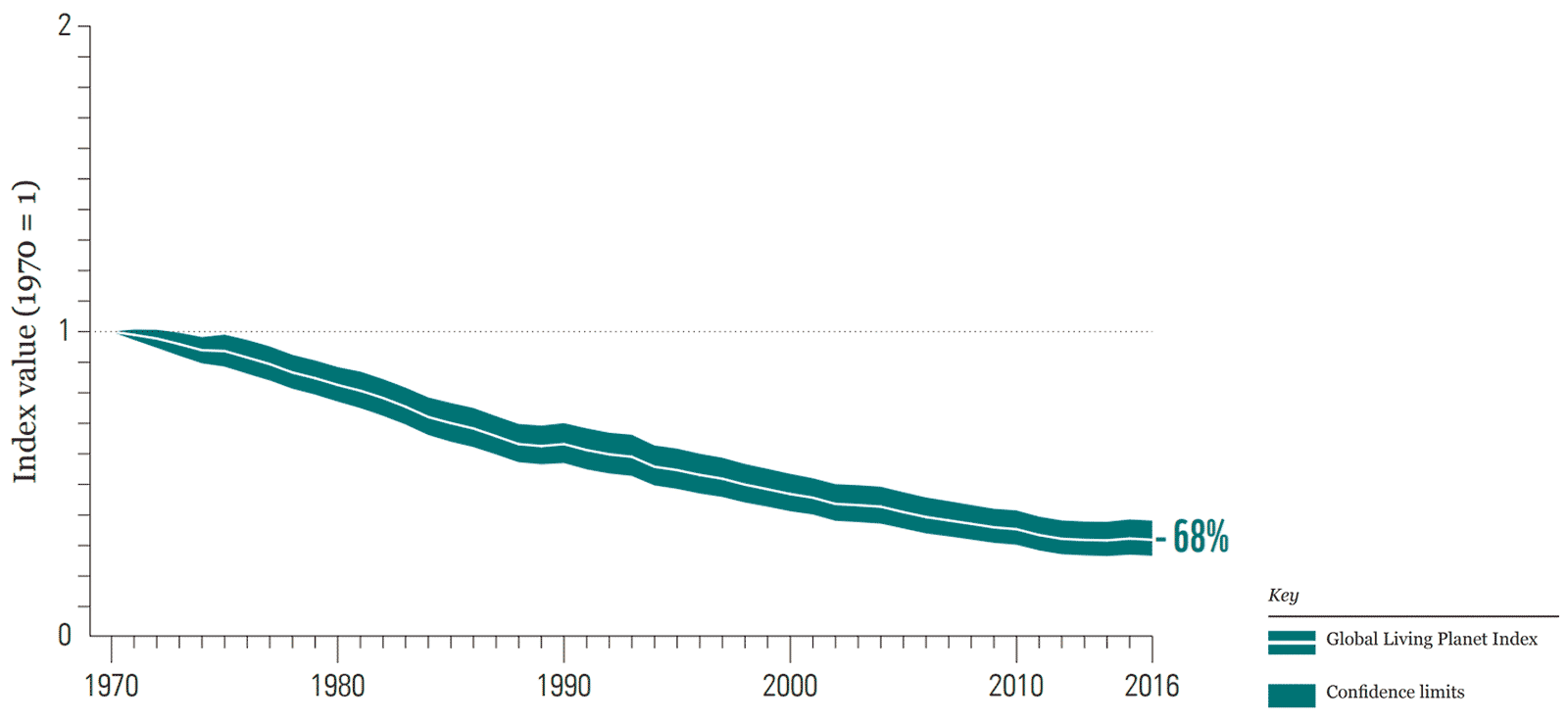

In parallel, WWF’s Living Planet Report 2020[ii] reveals that based on 4,392 species assessments, global populations of vertebrate species have declined by an average of 68 per cent since 1970 – see Figure 1.

Figure 1: The global Living Planet Index: 1970 to 2016 Average abundance of 20,811 populations representing 4,392 species monitored across the globe.[iii]

Both of these reports cite habitat destruction and degradation, deforestation, overfishing and climate change as major drivers of biodiversity loss.

Partially enabling these drivers in 2019, public subsidies deemed harmful to nature[1] amount to between US$895bn and US$978bn including to the fossil fuel industry.[iv] Financing Nature: Closing the global biodiversity financing gap estimates that global subsidies damaging nature for agriculture (for example subsidies supporting monocultures or excessive fertilizer application) amounted to US$451bn, forestry US$55bn and fisheries US$36bn.

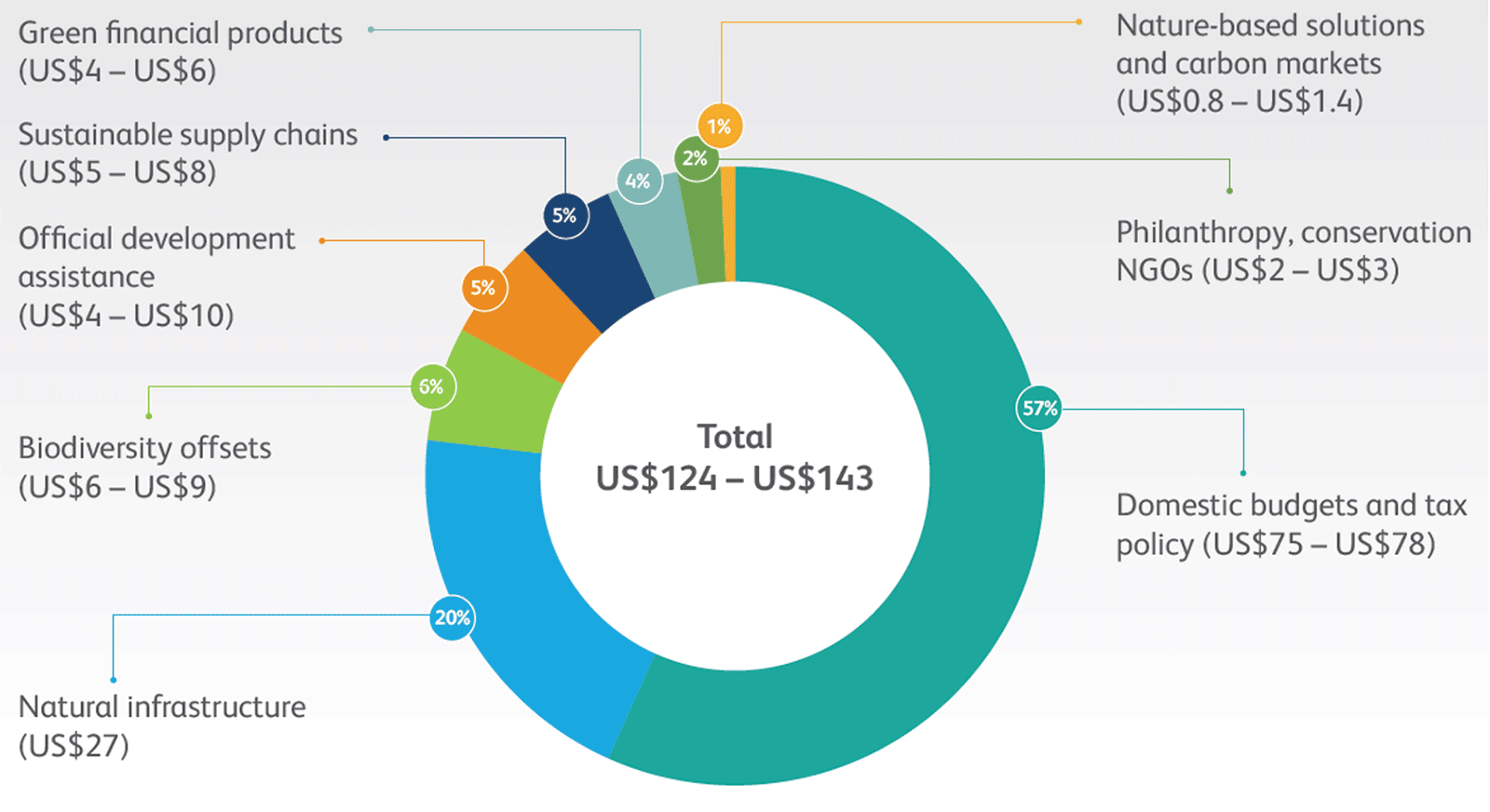

By contrast, annual global public and private biodiversity funding supporting biodiversity conservation between 2015 and 2019 amounted to between US$78bn and US$143bn – see Figure 2. [v],[vi]

In other terms, total annual public and private funding supporting biodiversity conservation is outstripped by harmful subsidies in agriculture, forestry and fisheries by between 3.5x to 6.4x.

Figure 2: Global biodiversity conservation financing in 2019: Summary of financial flows into biodiversity conservation.[vii]

To slow, and in certain cases stop, the decline of biodiversity, will require between US$598bn and US$824bn per annum. In 2014, Credit Suisse and McKinsey estimated this gap to be US$300bn to US$400bn, suggesting a spread increase between 99 and 106 per cent in just six years.[viii]

‘Biodiversity finance’ mechanisms mentioned in Financing Nature: Closing the global biodiversity financing gap such as biodiversity offsets can contribute towards bridging this gap. Most of these options, however, remain too niche, lack supportive policies and regulation enabling them to scale, and as yet are not widely known to mainstream capital markets.

With the public domestic expenditure biodiversity finance gap to 2030 estimated by the OECD to be US$67.8bn, for the short- to mid-term at least, niche biodiversity finance is unlikely to meaningfully generate the capital required to halt biodiversity declines.[ix]

Clearly it is important to scale up biodiversity finance. But the proposed biodiversity finance mechanisms alone are insufficient: it would be like trying to solve climate change only by investing in renewables, whereas the key to net zero is also eliminating investment in fossil fuels.

Likewise, with biodiversity, policy makers and financiers need to be focused as much on the trillions already in the financial system that take no account of biodiversity, as well as the billions that need to be directed to specific conservation efforts. As those on a diet know, eating salad is fine; you need to exclude the cakes as well.

However, the diet is yet to begin. In 2020, ShareAction undertook a survey to assess the approach to biodiversity of 75 of the world’s largest asset managers that collectively hold over US$56 trillion in assets under management. The results found that none of the assessed asset managers has a stand-alone, dedicated policy on biodiversity covering all portfolios under management.[x]

These finance and stewardship gaps point towards an urgent need for structural interventions which are applicable to mainstream global capital markets and at financial scale. Interventions such as eliminating public subsidies which degrade biodiversity; mobilising central banks and supervisors to address the prudential and monetary risks of biodiversity loss; and aligning capital markets with regeneration biodiversity, notably bank lending, equities and fixed income are essential to mount a credible challenge at the biodiversity crisis.

Fixed income markets potentially offer the largest biodiversity finance opportunity

Planet Tracker has previously demonstrated the wider financial system dependencies on biodiversity as part of natural capital – see for example the LSE and Planet Tracker award-winning report The Sovereign Transition to Sustainability: Understanding the Dependence of Sovereign Debt on Nature[xi] pushing for natural capital factors to be fully incorporated into sovereign bond issuance; Can Blue Bonds Finance a Fish Stock Recovery[xii] and Ending deforestation: what next for sovereign investors?[xiii]

These papers highlight how existing fixed income markets are capable in the immediate term of mobilising significant conservation finance, hundreds of billions of dollars, including for biodiversity.

Existing macroeconomic and fixed income market dynamics currently support this assertion because:

- Interest rates: Central bank interest rates across most OECD countries are close to and in some cases below zero. This creates market demand particularly from pension funds for long dated lower yielding, relative to equities, financial instruments.

- Quantum and adaptability: The Institute of International Finance values global debt markets at over US$247 trillion. US debt markets are double the size of US equites. Unlike niche biodiversity finance mechanisms, sovereign and corporate debt including funds are familiar asset classes for capital markets. Financial institutions can relatively easily adapt or restructure existing debt instruments to support biodiversity, or issue new debt in the form of green bonds. Green bonds can support biodiversity via defined use of proceeds, revenue linked performance payments channelling bond interest towards biodiversity conservation and project finance. In 2020 (September year-to-date) US$134bn of new green bonds have been issued with existing global green issuances exceeding US$1tn according to the Climate Bonds Initiative. Whilst green bonds currently represent a minor portion of overall bond markets, with US$350bn of new sovereign and corporate green bond issuances forecast in 2020, the upward trend points towards a credible financing option to bridge the biodiversity finance gap.[xiv]

- Liquidity: Bond markets offer investors liquidity often not available with niche biodiversity finance instruments.

- Creditworthiness: Risk of debt instruments is ranked by rating agencies making them eligible for low risk investors such as pension funds. The ability to protect principal (par value) whilst generating regular income (annuity payments) is another attractive feature of fixed income instruments for investors.

- Debt Maturities: Debt can be structured across short- to long-term maturities making fixed income suitable for funding longer dated projects supporting biodiversity and climate recovery such as reflooding peatlands, afforestation and fisheries recovery. Debt offers a flexible financing option, over equity, enabling variable coupons, principal holidays and mezzanine options.

- Contracts: Bond term sheets, which layout the basic terms and conditions of the investment, can include biodiversity measures such as soil quality, along with the usual conditions such as amount raised, interest rate, payment dates and maturity dates.

In the future, reports such as the UN CBD Global Biodiversity Outlook 5 and Financing Nature: Closing the global biodiversity financing gap would benefit from exploring in more depth how ‘mainstream’ fixed income instruments such as sovereign debt restructuring, new green bond issuances and green conditional project loans could be used or adapted to bridge the biodiversity funding gap.

Momentum is building to mobilise more biodiversity funding but practitioners cannot afford to ignore existing capital market opportunities, particularly fixed income, if they are serious about bridging the finance deficit.

[1] Subsidies are environmentally harmful, if the activities supported by the subsidy (production, consumption, transport etc.) have more detrimental effects on the environment than the activities displaced by the effects of the subsidy. Schweppe-Kraft, B. (2009). Subsidies Harmful to Biodiversity.

[i] Secretariat of the Convention on Biological Diversity (2020) Global Biodiversity Outlook 5. Montreal

[ii] WWF (2020) Living Planet Report 2020 – Bending the curve of biodiversity loss. Almond, R.E.A., Grooten M. and Petersen, T. (Eds). WWF, Gland, Switzerland.

[iii] WWF (2020) Living Planet Report 2020 – Bending the curve of biodiversity loss. Almond, R.E.A., Grooten M. and Petersen, T. (Eds). WWF, Gland, Switzerland.

[iv] Perry, E., et al. (2020). A Comprehensive Overview of Global Biodiversity Finance.

[v] Deutz, A., Heal, G. M., Niu, R., Swanson, E., Townsend, T., Zhi L., Delmar, A., Meghji, A., Sethi, S. A., and Tobin-de la Puenta, J. 2020. Financing Nature: Closing the global biodiversity financing gap. The Paulson Institute, The Nature Conservancy and Cornell Atkinson Center for Sustainability.

[vi] Secretariat of the Convention on Biological Diversity (2020) Global Biodiversity Outlook 5. Montreal

[vii] Deutz, A., Heal, G. M., Niu, R., Swanson, E., Townsend, T., Zhi L., Delmar, A., Meghji, A., Sethi, S. A., and Tobin-de la Puenta, J. 2020. Financing Nature: Closing the global biodiversity financing gap. The Paulson Institute, The Nature Conservancy and Cornell Atkinson Center for Sustainability.

[viii] Deutz, A., Heal, G. M., Niu, R., Swanson, E., Townsend, T., Zhi L., Delmar, A., Meghji, A., Sethi, S. A., and Tobin-de la Puenta, J. 2020. Financing Nature: Closing the global biodiversity financing gap. The Paulson Institute, The Nature Conservancy and Cornell Atkinson Center for Sustainability.

[ix] Perry, E., et al. (2020). A Comprehensive Overview of Global Biodiversity Finance.

[x] Springer, K. (2020). Point of No Returns Part IV – Biodiversity. An assessment of asset managers’ approaches to biodiversity.

[xi] Pinzón A and Robins N with McLuckie M and Thoumi G (2020) The sovereign transition to sustainability: Understanding the dependence of sovereign debt on nature. London: Grantham Research Institute on Climate Change and the Environment, London School of Economics and Political Science, and Planet Tracker.

[xii] Mosnier, F., et al (2020). Can Blue Bonds Finance a Fish Stock Recovery.

[xiii] Robins, N., et al (2020). Ending Deforestation: What Next for Sovereign Investors?

[xiv] Climate Bonds Initiative (September 2020). https://www.climatebonds.net/