These predictions for 2022 from the Planet Tracker Team are specifically relevant to the global financial markets.

- An underperformance of ESG funds – will sector rotation dominate?

- A slowdown in the growth of green bond issuances – will quality win over quantity?

- A rising number of corporates demerging green assets.

- Traceability will become the norm, not the exception.

- Commodities linked to deforestation are likely to present a material risk to profits.

- Retail investors to win direct voting rights.

- Executives likely to face more scrutiny and challenge on pay.

- ESG to underperform – will sector rotation dominate?

Many ESG funds, the majority being climate-focused, typically have a sectoral bias. More often than not they are overweight with technology, communication services[i] and healthcare[ii] stocks and underweight energy, real estate and industrials companies. Both active and passive climate funds aim to identify companies which have low carbon footprints and have potential to create high shareholders returns.[iii] As a result in the year to July 2021, 8 of the 10 best performing US ESG funds had either Apple, Amazon or Microsoft as their biggest holding.[iv] However, a number of companies in the energy, utility and real estate sectors[v] are often absent or have minimal weightings in ESG funds because of their significant carbon footprints. The exceptions are the renewable energy and utility companies which will obviously form an important part of many ESG fund portfolios.

With more than half of ESG funds outperforming the S&P 500 in the first five months of 2021[vi] should investors worry about a reversal in these fortunes in 2022?

Potentially yes. A turnaround in the performance of these sectors – i.e. a tech sector sell-off and a strong energy/utility resurgence – could impact ESG fund performance given their exposure to tech. In addition to this if inflation persists, non-ESG funds could buy into the energy sector as an inflation hedge increasing energy company share prices[vii] but inflation could also drive up the costs for renewable companies – solar panels and wind turbines, for example – leaving them less well off than their non-sustainable fossil fuel competitors and hurting ESG fund valuations as a result. ESG and sustainable portfolio managers will need to be agile if they are to outperform in the face of such financial market shifts.

- Green Bond Issuances to slow – quality over quantity?

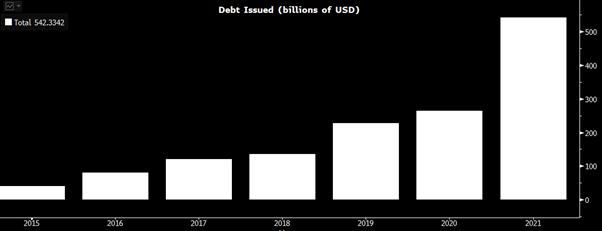

Green bonds have had a stellar rise in issuances in recent years. The market pushed through USD 1 trillion in cumulative issuances (since inception) in December 2020 according to Climate Bonds Initiative (CBI).[viii] Furthermore, in 2021 we reached USD 540 million of new issuances, more than double 2020.

Figure 1: Green Bond Issuances since 2015 – Bloomberg

We believe the pace of green bonds issuances could slow for three main reasons:

- Regulatory scrutiny will increase: A Competition and Markets Authority (CMA) review found that as much as 40% of firms’ green claims could be misleading.[ix] Financial institutions are likely to be more cautious before buying such instruments; green credentials will need to be robust. Increased regulatory scrutiny will force issuers and underwriters to increase the quality of the issuances; this will improve trust in the market and reduce the amount of greenwashing.

- Underperformance: recent data compiled by Bloomberg reveals Green Bonds down 3% this year versus the Bloomberg Investment-Grade Global Aggregate Index.[x] While a greenium (the spread of the green bond curve vs the issuer’s non-green or standard yield curve) provides an incentive for issuers by reducing their cost of issuing debt, investors may become unprepared to absorb this cost.

- Sustainability-linked Instruments better for issuers: a staggering tenfold growth in sustainability-linked bonds is being driven by the flexibility afforded issuers through not being tied by the Use-of-Proceeds rule, unlike other sustainable bonds. We expect their popularity to continue but investor and regulatory scrutiny of the embedded sustainability targets is likely to increase.

Overall, we expect the slowdown in the green bond market growth rate to be a positive, with the market pivoting to quality over quantity. This will reduce the prevalence of greenwashing and bolster trust in the market. Sustainability-linked bonds, whilst more flexible, are likely to follow a similar path to their green siblings.

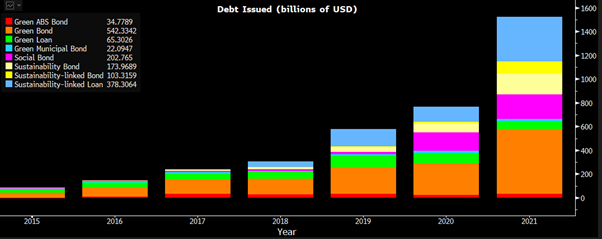

Figure 2: ESG-labelled Debt Market Issuances since 2015 – Bloomberg

- The year of the green spin-off

In the final months of 2021, investors witnessed three large industrial groups declare their intention to sell off divisions in an attempt to improve shareholder value: General Electric (Healthcare division), Johnson & Johnson (Consumer Healthcare division) and Toshiba (both Energy Infrastructure and Computer Devices). We believe management teams might consider similar spin-offs of their green assets given current high market valuations and the market’s enthusiasm for sustainable investment opportunities, particularly if those green assets appear undervalued as part of a larger industrial group or if sale proceeds could help finance a transition strategy.

Energy companies, whether utilities or oil & gas companies, are obvious protagonists. SSE, the UK utility, is resisting calls from Elliott Investment Management to split off its renewables business, while Shell has rebuffed New York–based hedge fund Third Point Management’s demand to sell its LNG and renewables activities. In contrast, ENI, the Italian energy company, has revealed plans to partially float its retail and renewable power business (Plentitude).

Of course, the push for a greener company could take a different direction by disposing of unsustainable assets, the equivalent of the financial sector’s ‘bad bank’ structure. For example, there is significant pressure for Glencore to sell its coal assets while BHP responded to activists by merging its oil & gas subsidiary with Woodside and distributing these new shares to BHP shareholders. Expect more corporate restructuring around green and sustainable themes.

- Traceability will become BAU

As companies and investors feel the increasing pressure to understand the environmental and social impacts of their supply chains (through the requirement to report Scope 3 emissions or through other corporate commitments), we expect a continuing focus on traceability for consumer facing companies and a continuing debate around what transparency should look like. Financial markets are becoming less and less forgiving when unethical and risky supply chain practices are unearthed. Technologies are now available to enable fully traceable and transparent supply chains.

The arguments for full supply chain traceability are indisputable – better traceability gives companies a better understanding of their supply chain and, through measurement, they are more able to identify where efficiencies can be improved (and costs saved) and operational risks managed. This is critical given the stress supply chains have been under over the last two years. This is, of course, also crucial for managing environmental impacts such as being able to identify areas of risk from climate change (and increasingly other nature related issues) and being able to manage and measure inputs (e.g. energy and water) and outputs (e.g. waste) to enable companies to meet their commitments on carbon emission reductions.

Over the next year, we expect a much wider implementation of traceability technologies to continue. With higher levels of inflation, price increases to fund supply chain investments would allow for profit margins to hold firm, removing the excuse that costs will not be recouped.

- EU regulation banning deforestation-linked imports – a material risk to earnings

Deforestation has long been on the sustainability agenda, with previous regulation having mixed effects. The new regulation on deforestation proposed by the European Commission on 17 November 2021[xi] to restrict products linked to deforestation from entering the bloc will, in Planet Tracker’s view, have a significant impact on companies importing to the EU. It will all be in the execution, but this regulation provides a direct risk to earnings and so should be high on investors’ agendas when engaging with exposed companies.

The regulation will initially target six commodities most linked to deforestation: coffee, cocoa, cattle, palm oil, soy and wood, as well as derived products. Under the new regulations, it will be illegal to sell or import any of the six commodities if they have been produced on deforested land converted after December 31, 2020.[xii] Companies, of all sizes, will need information on products sold in the EU to confirm they are deforestation free. The draft is yet to be approved by the EU Parliament and member countries (the EU Commission hopes to achieve this by 2023).

EU countries will be in charge of implementation and setting penalties. Punishments can include fines, seizure of the offending commodities, confiscation of revenues from their trade, as well as temporary exclusion of companies from public procurement. Compliance will be verified using satellite data and imagery with products banded into high, standard and low risk with more scrutiny applied to high-risk products/supply chains.[xiii]

- Retail investors to win direct voting rights

In 2019, Vanguard stated they would provide full proxy voting privileges to their external managers by 2020.[xiv] In 2021, the world’s largest asset manager, BlackRock, stated they will allow pension funds and institutional clients to directly vote in the annual meetings of nearly half of the USD 4.8 trillion equity index assets it manages.[xv] Increasingly, investors want a direct say on issues, but voting privileges are so far only being offered to institutional investors.

In 2021, US retail investors alone invested a record USD 1 trillion into equities worldwide, more than the last 20 years combined.[xvi], [xvii] 46% of retail investors aged 25-40 say they plan to vote their proxy votes in 2021 – the highest for any generation. Further, over 90% of the same age group would be more willing to vote if they could do so through a mobile app.[xviii] The survey also showed that diversity and environmental issues were the most important issues for this shareholder group.

Financial institutions have provided greater access for institutional investors to proxy vote in 2021. As retail investment in equities has hit an all-time high, asset managers looking to build on this enthusiasm and attract retail investors should leverage existing technology to provide voting access for retail investors in 2022. This will give an increasingly engaged and ESG focused shareholder group a voice in AGMs. We predict a move by one of the major investment managers.

- Executive pay will be challenged

We expect an increasing number of executive pay votes to be challenged by investors in 2022. We also anticipate the percentage of investors voting against executive pay packets to rise. The gap between executive pay and the average worker’s pay has widened significantly over the last 40 years and become more stretched during the COVID-19 pandemic.

The Economic Policy Institute estimates that CEO compensation has grown 1,322% since 1978, while the typical worker’s compensation has risen just 18%.[xix] This gap further widened, when the median pay ratio (the ratio of CEO pay to the median employee) for the largest 200 US companies by revenue was 274 to 1 in 2020, up from 245 to 1 in 2019.[xx]

With growing momentum behind companies’ social responsibility, we expect to see more executive pay packets being tied to ‘ESG’ performance. The US has been, and will most likely continue as, the laggard. Companies such as Schneider Electric in Germany have been market leaders in this tying a fifth of its CEO’s compensation to ESG metrics in 2020[xxi]. We expect increasing numbers of corporate leaders to be incentivised on ESG performance.

Five events to monitor in 2022

The international climate and nature agenda points to a busy 2022. Key events worth tracking include:

- Plastics will be front and centre at the United Nations Environment Assembly 5.2 in Kenya (28 February – 2 March), countries’ delegations will negotiate the fundaments for the creation of a Global Plastics Treaty (see our blog for further insight). Event link

- The long awaited second part of the United Nations Convention on Biological Diversity (CBD) COP15 will take place in China in the spring (25 April – 8 May) with the objective of adopting the Post-2020 Global Biodiversity Framework (see our blog on COP15 Part 1 for further insight). Event link

- XV World Forestry Congress in South Korea (2 – 6 May) will focus on six sub-themes, including reversing forest loss, sustainable use of nature-based solutions and forest resources, and forest monitoring and data collection. Event link

- The United Nation Ocean Conference hosted in Portugal (27 June – 1 July) will aim to curb marine pollution and garner commitments for responsible consumption of ocean resources.. Event link Furthermore, countries’ representatives are expected to convene in March 2022 to agree on the text of an international legally binding instrument under the United Nations Convention on the Law of Sea (UNCLOS) on the conservation and sustainable use of marine biological diversity of areas beyond national jurisdiction. Event link

- The United Nations Framework Convention on Climate Change (UNFCCC) COP27 in Egypt (7 – 18 November) will advance the global climate talks and, according to Egypt’s President Abdel Fattah al-Sisi, will be a “radical turning point in international climate efforts in co-ordination with all parties, for the benefit of Africa and the entire world”. Event link

[i] https://support.msci.com/documents/10199/4c7371c2-015a-cced-4eb6-fa0afb8a36a7

[ii] https://www.abrdn.com/en-us/us/investor/insights-thinking-aloud/article-page/esg-funds-show-their-mettle

[iii]https://news.mongabay.com/2021/04/behind-the-buzz-of-esg-investing-a-focus-on-tech-giants-and-no-regulation/

[iv] https://www.ft.com/content/ea295d51-d5c2-4916-8c63-017c352ea577

[v] https://support.msci.com/documents/10199/4c7371c2-015a-cced-4eb6-fa0afb8a36a7

[vi] https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/most-esg-funds-outperformed-s-p-500-in-early-2021-as-studies-debate-why-64811634

[vii] https://www.sharesmagazine.co.uk/news/shares/energy-and-resources-an-inflation-hedge

[viii] https://www.climatebonds.net/2020/12/1trillion-mark-reached-global-cumulative-green-issuance-climate-bonds-data-intelligence

[ix] https://www.gov.uk/government/news/global-sweep-finds-40-of-firms-green-claims-could-be-misleading

[x] https://www.bnnbloomberg.ca/esg-bond-buyers-swallow-short-term-losses-to-gain-ethical-kudos-1.1697288

[xi] Regulation of the European Parliament and of the Council on the making available on the Union market as well as export from the Union of certain commodities and products associated with deforestation and forest degradation and repealing Regulation (EU) No 995/2010.

[xii] https://www.euractiv.com/section/energy-environment/news/europe-proposes-mandatory-due-diligence-to-stop-deforestation-in-supply-chains/

[xiii] https://www.politico.eu/article/commission-adds-new-wrinkle-to-lifestyle-choices-deforestation/

[xiv] https://www.irmagazine.com/buy-side/vanguard-gives-proxy-voting-decision-powers-external-managers

[xv] https://www.ft.com/content/4e8a4b14-3450-4be3-8526-2cc184f0ebfe

[xvi] https://www.ft.com/content/64995a1c-ebc5-4177-8866-9727fdfbdcb1

[xvii] https://markets.businessinsider.com/news/stocks/stock-market-retail-investors-trillion-jpmorgan-trading-activity-levels-meme-2021-6

[xviii] https://www.irmagazine.com/shareholder-targeting-id/retail-investors-millennials-most-likely-vote-their-proxy-finds-new-survey

[xix] https://www.epi.org/publication/ceo-pay-in-2020/

[xx] Huge Paydays for C.E.O.s, as Gap With Workers Widened – The New York Times (nytimes.com)

[xxi] https://www.ft.com/content/c1d0e4d5-b42f-4287-8bfe-319f31a7acbe